How insurance leaders can overcome fear, bias and ignorance to make innovation actually happen

Insurance innovation fails not because companies lack ideas or budget. It fails because the organizational immune system attacks anything unfamiliar. And that immune system is made entirely of people. Understanding why that happens is the first step to overcoming it.

Fear: The Innovation Killer in Insurance

Fear in large insurers is rational, not irrational — which makes it harder to dismiss. Underwriters fear that a failed experiment reflects on their judgment. Actuaries fear signing off on models they can’t fully validate. Middle managers fear that a successful innovation will reorganize their team out of existence.

The antidote isn’t courage speeches. It’s psychological safety backed by structural protection — meaning experiments are formally decoupled from performance reviews, failure is documented and shared openly as learning, and leaders visibly absorb blame when things go wrong rather than passing it down.

At Curium, we see this play out with clients regularly. The conversations that lead to real change rarely start with technology — they start with someone finally feeling safe enough to say “this process has never made sense.”

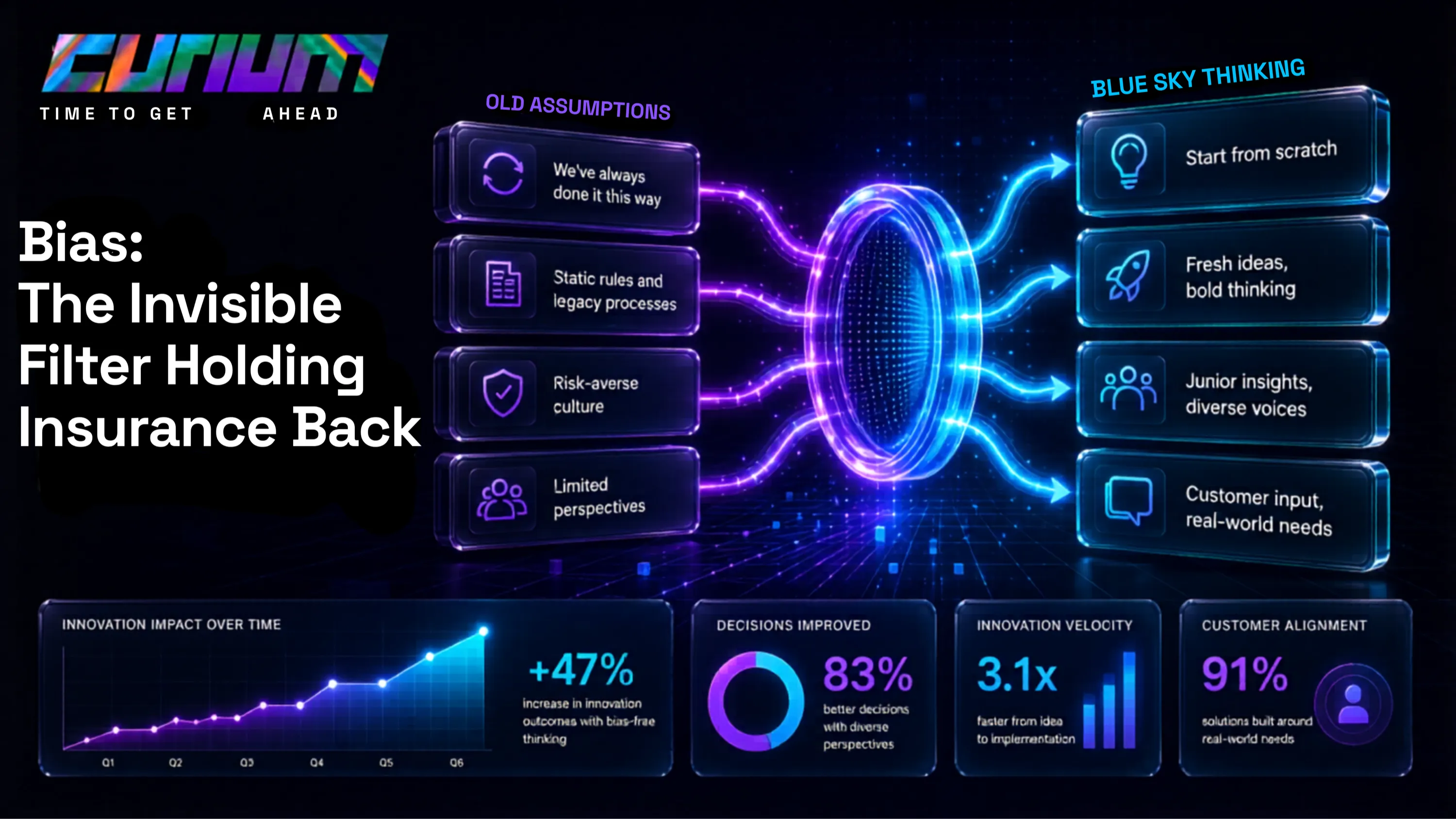

Bias: The Invisible Filter Holding Insurance Back

Incumbency bias is brutal in insurance. “We’ve always priced it this way” is treated as wisdom rather than inertia. Successful underwriters and actuaries built careers on a set of assumptions — asking them to invalidate those assumptions is asking them to undermine their own authority.

The move here is separating evaluation from execution. Bring in outside perspectives — from adjacent industries, from customers, from junior staff — specifically to challenge assumptions. This is why we regularly run blue sky thinking sessions with our clients: structured conversations where the rules of the existing system are temporarily suspended, and people are asked what they would build if they were starting from scratch. The ideas that emerge from those sessions have directly shaped features we’ve gone on to build. The best product innovations don’t come from sitting in a room guessing — they come from listening carefully to people who live inside the problem every day.

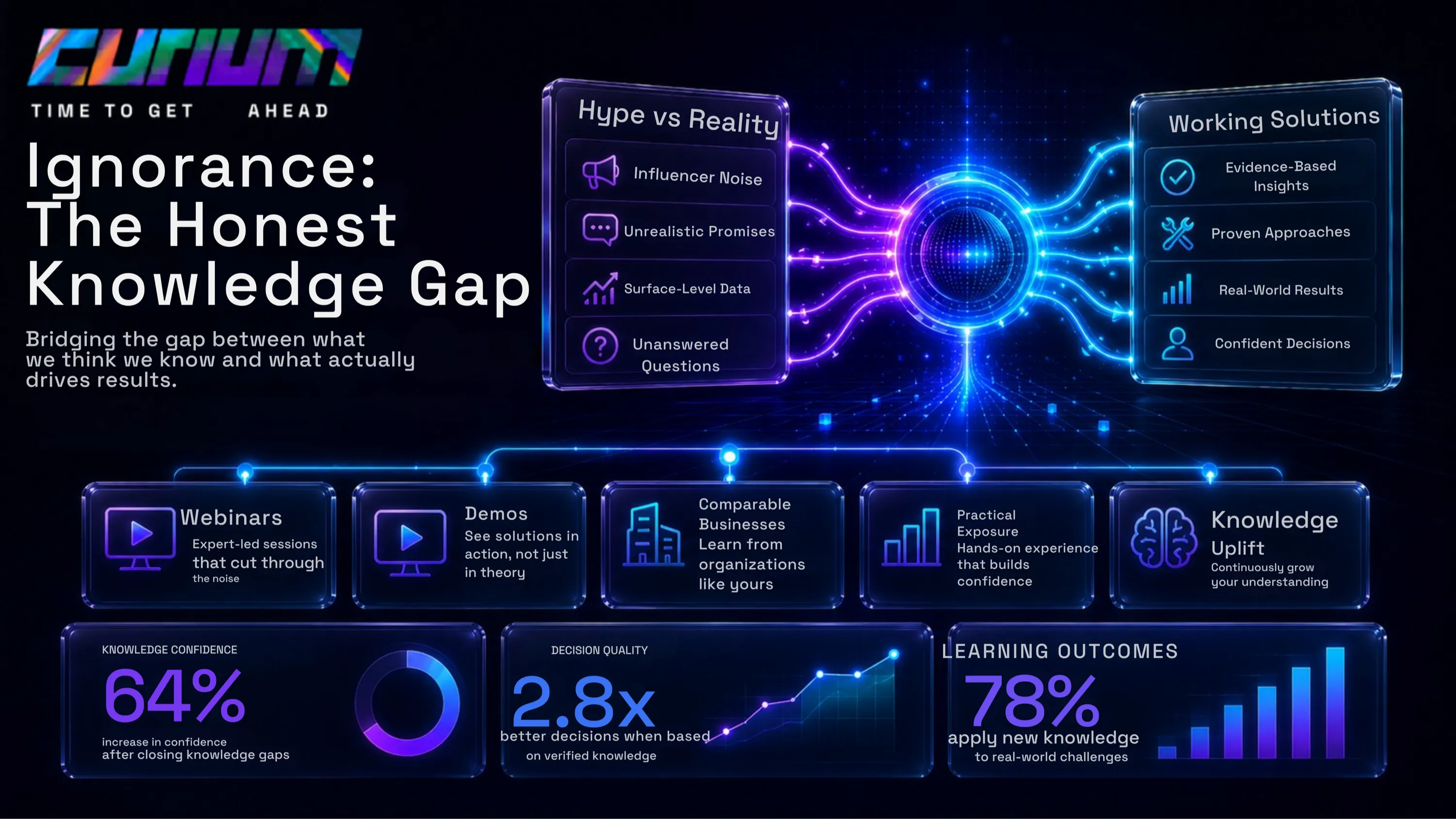

Ignorance: The Honest Knowledge Gap

Many insurance leaders genuinely don’t know what modern technology can and can’t do. This creates two failure modes: dismissing real possibilities as hype, or chasing hype without understanding the limits. Both are expensive.

This is a big part of why we run regular webinars — not to sell, but to close the gap through sustained, practical exposure. When people see what’s actually working in comparable businesses, the conversation shifts from “is this possible?” to “why haven’t we done this yet?” Proximity to working solutions is a far more powerful educator than any training deck.

Build the Conditions for Innovation, Not Just the Ideas

Beyond the three blockers, organizational conditions matter enormously:

• Ring-fence the budget. Innovation that competes with core business operations for funding will always lose. Separate the money and you separate the politics.

• Name your tolerance for failure. If leadership explicitly accepts that one in three experiments won’t work — and means it — behavior changes immediately. If it’s never said, people assume zero tolerance and act accordingly.

• Stay close to the real problem. Abstract innovation labs disconnected from operations almost always wither. The best innovations come from people closest to the pain — give them permission and resources, not a separate building.

• Never rely on gut feel when facts are available. In insurance, facts are almost always available. This discipline matters most when new regulations land. Gut feel about what a regulator means is how companies end up with material breaches. Going back to the actual obligation, the actual data, the actual evidence is what separates organizations that lead on compliance from those that scramble to catch up.

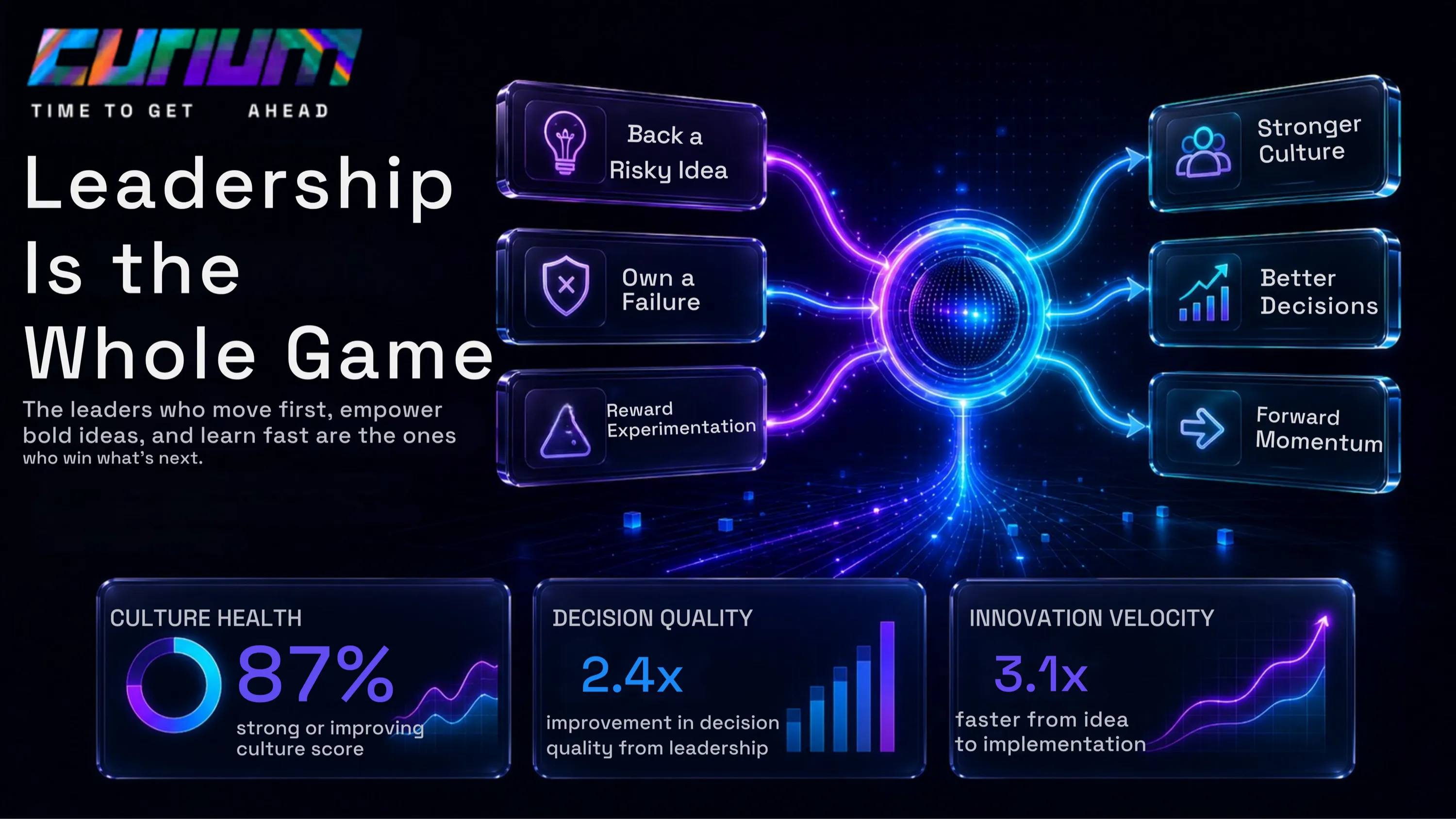

Leadership Is the Whole Game

None of this works without leaders who model the behavior they want. If a CEO talks about innovation but kills anything uncertain in budget reviews, the organization reads the behavior, not the speech.

The most powerful thing a senior leader can do is publicly back a risky idea, publicly own a failure, and publicly reward someone who tried something that didn’t work. Those three acts do more for an innovation culture than any strategy document ever written.

Insurance innovation is less an R&D problem and more a leadership and culture problem dressed up as a technology problem. The companies getting it right aren’t necessarily the ones with the biggest budgets — they’re the ones where someone in a position of authority decided that the cost of staying still was higher than the cost of trying something new.

At Curium, we work through these challenges alongside our clients — through webinars, blue sky sessions, and technology built directly from what we learn together. If your team is ready to have the honest conversation, we’d love to be in the room.

Author:

Tetiana George, CEO of Curium, Co-Chair of Insurtech Australia and member of ASIC Digital Finance Advisory Committee. LinkedIn Profile.